Markets2026.04.30

Stagnant Growth, Rising Prices: What America's Stagflation Return Means for Global Markets

저성장·고물가의 귀환: 미국의 스태그플레이션이 글로벌 시장에 던지는 질문

The Return of a 1970s Nightmare

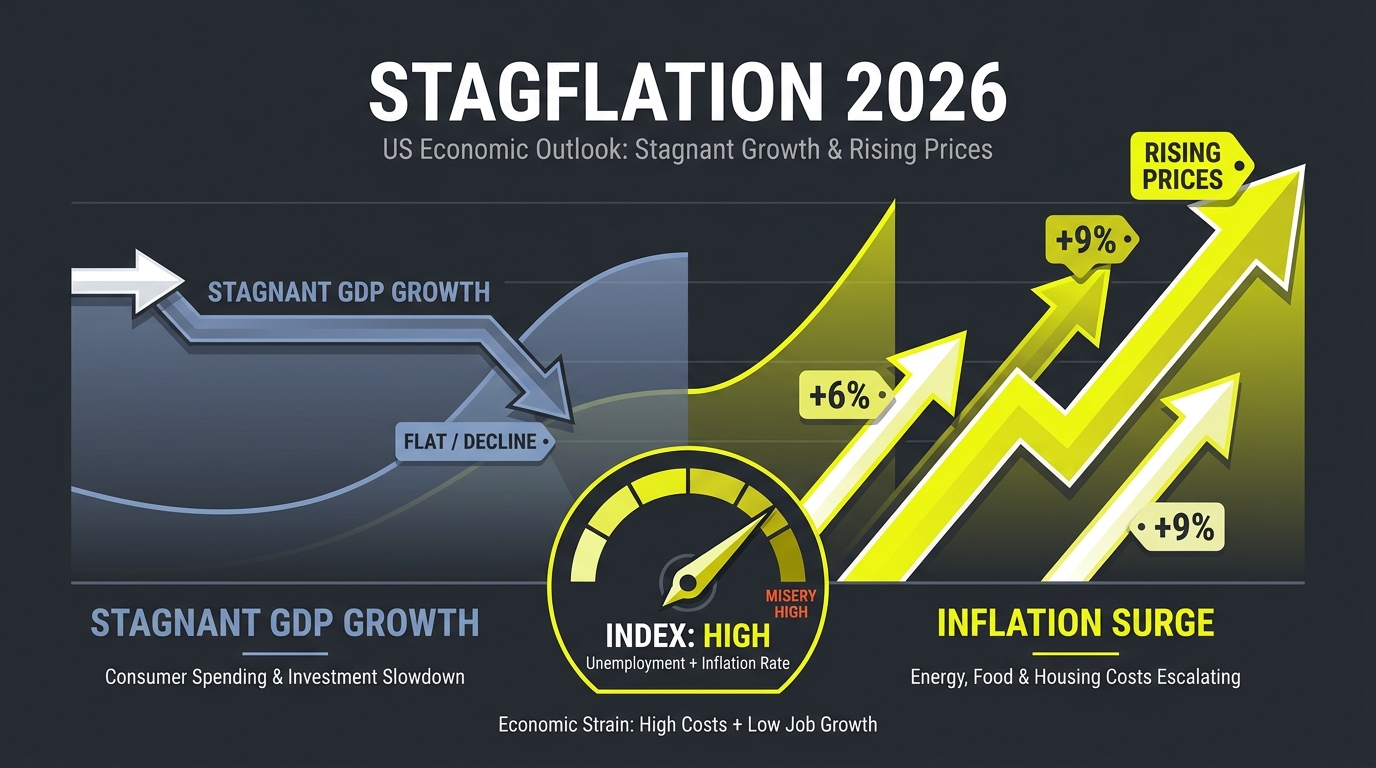

The U.S. economy shrank in the first quarter of 2026 — and yet prices are still rising. That combination, once thought to be a relic of the 1970s, has a name that markets are using again with alarm: . On Wednesday, the U.S. Bureau of Economic Analysis reported that gross domestic product contracted at an annualized rate of 0.3% in Q1 2026. The contraction surprised economists who had expected 1.1% growth, and it sent the S&P 500 down 2.1% and the Dollar Index below 97 — its weakest level since 2022.

2026년 1분기, 미국 경제가 위축되었습니다. 그런데 물가는 여전히 오르고 있습니다. 한때 1970년대의 유물로 여겨졌던 이 조합에는 이름이 있습니다. 시장이 다시 우려와 함께 꺼내 드는 단어, 스태그플레이션(stagflation)입니다. 수요일, 미국 경제분석국(BEA)은 2026년 1분기 국내총생산(GDP)이 연율 기준 0.3% 수축(contraction)했다고 발표했습니다. 이 수치는 1.1% 성장을 예상했던 이코노미스트들을 놀라게 했고, S&P 500을 2.1% 끌어내리며 달러 인덱스를 2022년 이후 최저치인 97 아래로 밀어 넣었습니다.

Why Stagflation Is Uniquely Dangerous

The word "" blends "stagnation" and "inflation." It describes an economy stuck in the worst of both worlds: growth is slowing or reversing, while prices continue to rise. This is particularly troubling because the standard policy tool for fighting each problem works against the other. Raise interest rates to fight inflation — and you risk making the recession worse. Cut rates to stimulate growth — and you risk making inflation worse. The Fed's preferred inflation gauge — the (Personal Consumption Expenditures) price index — remained elevated at 3.1% in Q1, well above the 2% target. Combined with the GDP contraction, this pushed the so-called misery index — the sum of the unemployment rate and the inflation rate — to its highest reading since 1983, a number that captures how painful economic conditions feel for ordinary households.

'스태그플레이션'이라는 단어는 '침체(stagnation)'와 '인플레이션(inflation)'의 합성어입니다. 최악의 상황이 동시에 벌어지는 경제를 묘사합니다. 성장은 둔화되거나 역전되는데 물가는 계속 오르는 것입니다. 이것이 특히 위험한 이유는, 각각의 문제를 해결하는 표준 정책 수단이 서로를 악화시키기 때문입니다. 인플레이션을 잡으려고 금리를 올리면 경기 침체가 심해질 위험이 있고, 성장을 촉진하려고 금리를 내리면 인플레이션이 더 심해질 위험이 있습니다. 연준이 선호하는 인플레이션 지표인 PCE(개인소비지출) 가격지수는 1분기에 3.1%로 목표치 2%를 크게 웃돌았습니다. GDP 수축과 맞물려, 이른바 미저리 인덱스(misery index) — 실업률과 인플레이션율의 합 — 가 1983년 이후 최고치를 기록했습니다. 이 수치는 일반 가계가 경제 상황을 얼마나 고통스럽게 느끼는지를 단적으로 보여줍니다.

The Fed Caught Between Two Fires

The Federal Reserve now faces what economists call a classic monetary policy dilemma. Before Wednesday's data, markets were pricing in only a 25% chance of a June rate cut. After the GDP print, that probability jumped to 60%. Yet cutting rates risks reigniting inflation that the Fed has spent two years trying to bring under control. The Fed is caught between two fires.

연방준비제도(Fed)는 이제 경제학자들이 고전적 통화정책 딜레마(monetary policy dilemma)라고 부르는 상황에 처했습니다. 수요일 데이터 발표 전, 시장은 6월 금리 인하 가능성을 25%로만 반영했습니다. GDP 수치 발표 후 그 확률은 60%로 치솟았습니다. 그러나 금리를 내리면 2년간 잡으려 애써온 인플레이션이 재점화될 위험이 있습니다. 연준은 두 개의 불 사이에 갇혀 있습니다.

When Bonds Behave Badly: The Bear Steepener

Unusually, the bond market sent a counterintuitive signal on Wednesday. Long-term Treasury yields rose rather than fell after the weak GDP report — a phenomenon known as a bear steepener. In normal recessions, bad growth data drives investors into the safety of government bonds, pushing yields down. But this time, investors are more worried about the U.S. fiscal deficit — now projected at $2.1 trillion — than they are reassured by safe-haven demand for Treasuries. The force pushing yields up despite weak growth has a name: term premium — the extra return investors demand to compensate for the risk of holding long-duration government debt. When fiscal deficits are large and growing, term premium rises, because investors fear that governments may need to issue even more bonds to fund their spending, diluting the value of existing bondholders' holdings. When the fiscal deficit becomes so large that it begins to constrain the central bank's ability to fight inflation freely — because raising rates dramatically worsens the government's own borrowing costs — economists call this fiscal dominance. It is a condition in which the government's financing needs override the central bank's inflation mandate, a trap that historically has led to prolonged periods of above-target inflation.

이례적으로, 채권 시장은 수요일 직관에 반하는 신호를 보냈습니다. 부진한 GDP 발표 이후 장기 국채 금리가 하락하지 않고 오히려 상승했습니다. 베어 스티프너(bear steepener)라 불리는 현상입니다. 일반적인 경기침체에서는 부진한 성장 데이터가 투자자들을 국채 안전자산으로 유도해 금리를 낮춥니다. 그러나 이번에는 투자자들이 2조 1천억 달러로 예상되는 미국 재정 적자를 국채의 안전자산 매력보다 더 우려하고 있습니다. 성장 부진에도 불구하고 금리를 끌어올리는 힘에는 이름이 있습니다. 기간 프리미엄(term premium)입니다. 장기 국채를 보유하는 위험에 대한 보상으로 투자자들이 요구하는 추가 수익률입니다. 재정 적자가 크고 계속 늘어날 때 기간 프리미엄은 상승합니다. 정부가 지출 자금을 마련하기 위해 채권을 더 많이 발행해야 할 수도 있어, 기존 채권 보유자들의 가치가 희석될 것을 투자자들이 우려하기 때문입니다. 재정 적자가 너무 커져 중앙은행이 자유롭게 인플레이션과 싸우는 능력을 제약하기 시작할 때 — 금리를 크게 올리면 정부 자신의 차입 비용도 악화되기 때문에 — 경제학자들은 이를 재정 지배(fiscal dominance)라고 부릅니다. 정부의 자금 조달 필요성이 중앙은행의 인플레이션 목표를 압도하는 상태로, 역사적으로 목표 이상의 인플레이션이 장기간 지속되는 함정으로 이어졌습니다.

The Stagflation Trade: How Investors Are Repositioning

How are investors responding? A clear " trade" is taking shape. Money is flowing out of growth stocks — the Nasdaq fell 2.8% Wednesday — and into assets that protect against inflation. Chief among them are (Treasury Inflation-Protected Securities), U.S. government bonds whose principal value adjusts with inflation, making them a direct hedge against rising prices even when nominal bond yields are rising. The broader portfolio shift is called sector rotation — the movement of money from sectors that perform well in one economic environment to sectors better suited for another. In a regime, investors typically favor energy producers (who benefit from high commodity prices), gold miners, and dividend-paying value stocks — and sell technology, consumer discretionary, and other rate-sensitive growth companies. Wednesday's market moves followed this playbook precisely. In South Korea, institutional investors are pursuing an adapted playbook: overweighting semiconductor and battery manufacturers supplying the AI infrastructure buildout, on the thesis that AI capex demand provides a demand floor relatively insensitive to the consumer spending slowdown driven by US tariff uncertainty. Individual Korean investors face a more difficult calibration: domestic bonds are now yielding near 4% after Bank of Korea rate hikes, which is competitive with dividend yields on blue-chip stocks, but the inflation outlook makes fixed-rate bonds risky if price pressures persist beyond 2026 — a scenario the IMF's latest World Economic Outlook considers more likely than not. The historical precedent from 1970s is instructive but imperfect: in that era, commodities and real assets performed well while financial assets struggled, but the 2026 economy has structural differences — AI-driven productivity improvements, a more globally integrated supply chain, and a different central bank policy framework — that make a simple 1970s playbook unreliable.

투자자들은 어떻게 반응하고 있을까요? 명확한 '스태그플레이션 트레이드'가 형성되고 있습니다. 자금이 성장주에서 빠져나와 — 나스닥은 수요일 2.8% 하락 — 인플레이션을 방어하는 자산으로 이동하고 있습니다. 그 중심에는 TIPS(물가연동국채, Treasury Inflation-Protected Securities)가 있습니다. 원금이 인플레이션에 연동해 조정되는 미국 국채로, 명목 채권 금리가 오를 때도 물가 상승에 대한 직접적 헤지 수단이 됩니다. 더 넓은 포트폴리오 이동은 섹터 로테이션(sector rotation)이라 불립니다. 어떤 경제 환경에서 잘 작동하는 섹터에서 다른 환경에 더 맞는 섹터로 자금이 이동하는 것입니다. 스태그플레이션 국면에서 투자자들은 보통 에너지 생산업체(원자재 고가격의 수혜자), 금광 기업, 배당형 가치주를 선호하고 기술주, 임의소비재, 기타 금리 민감 성장주를 팝니다. 수요일의 시장 움직임은 이 공식을 정확히 따랐습니다. 한국에서 기관 투자자들은 적응된 스태그플레이션 플레이북을 추구하고 있어요. AI 인프라 구축에 공급하는 반도체 및 배터리 제조업체를 과대 비중으로 가져가는 거예요. AI 설비투자 수요가 미국 관세 불확실성이 촉발한 소비자 지출 둔화에 비교적 둔감한 수요 바닥을 제공한다는 논제를 바탕으로요. 한국 개인 투자자들은 더 어려운 보정을 직면하고 있어요. 한국은행의 금리 인상 이후 국내 채권은 현재 약 4% 수익률을 제공하고 있어요. 이는 우량주의 배당 수익률과 경쟁적이에요. 하지만 인플레이션 전망은 가격 압박이 2026년 이후에도 지속된다면 고정금리 채권을 위험하게 만들어요. IMF의 최신 세계경제전망이 그럴 가능성이 더 높다고 보는 시나리오예요. 1970년대 스태그플레이션의 역사적 선례는 교훈적이지만 불완전해요. 그 시대에는 원자재와 실물 자산이 잘 수행된 반면 금융 자산은 어려움을 겪었지만, 2026년 경제는 구조적 차이가 있어요. AI 주도 생산성 향상, 더 글로벌하게 통합된 공급망, 다른 중앙은행 정책 체계가 1970년대 플레이북을 단순히 적용하는 것을 신뢰하기 어렵게 만들어요.

What to watch

For global markets, a stagflating U.S. economy creates a complex chain of consequences. A weaker dollar benefits emerging market countries that borrow in dollars — their debt becomes cheaper to service — but it also raises inflation in commodity-importing nations. South Korea, which exports heavily to the U.S. and runs a large trade surplus with it, faces both reduced export demand and won appreciation that squeezes corporate earnings. Watch for whether the Fed pauses its rate-cut path while inflation stays above 3% — if growth keeps slowing at the same time, that combination would be the clearest signal yet that the low-inflation regime of the past decade is truly over, and that portfolios built on those assumptions need rethinking.

글로벌 시장에 있어 스태그플레이션에 빠진 미국 경제는 복잡한 결과의 연쇄를 만들어냅니다. 달러 약세는 달러로 차입한 신흥국에게 유리합니다. 부채 상환 부담이 줄어들기 때문입니다. 그러나 동시에 원자재 수입국에서는 인플레이션을 높입니다. 미국에 대한 수출 비중이 크고 대미 무역 흑자를 보유한 한국은 수출 수요 감소와 기업 실적을 압박하는 원화 강세 모두에 직면합니다. 연준이 인플레이션 3%대에서도 금리 인하를 멈추는지 지켜보세요. 같은 시간에 성장까지 계속 둔화된다면, 그것이 바로 지난 10년의 저인플레이션 체제가 진정으로 끝났다는 가장 명확한 신호예요. 그 가정 위에 쌓아올린 여러분의 포트폴리오를 재점검할 때라는 뜻이기도 하고요.