Business2026.05.03

Why Anxiety Is Driving Gen Z Into the Stock Market

두려움이 젠지를 주식 시장으로 이끄는 이유

Intro

The New Investor Opens an App, Not a Savings Account

새로운 투자자는 저축 통장 대신 앱을 열어요

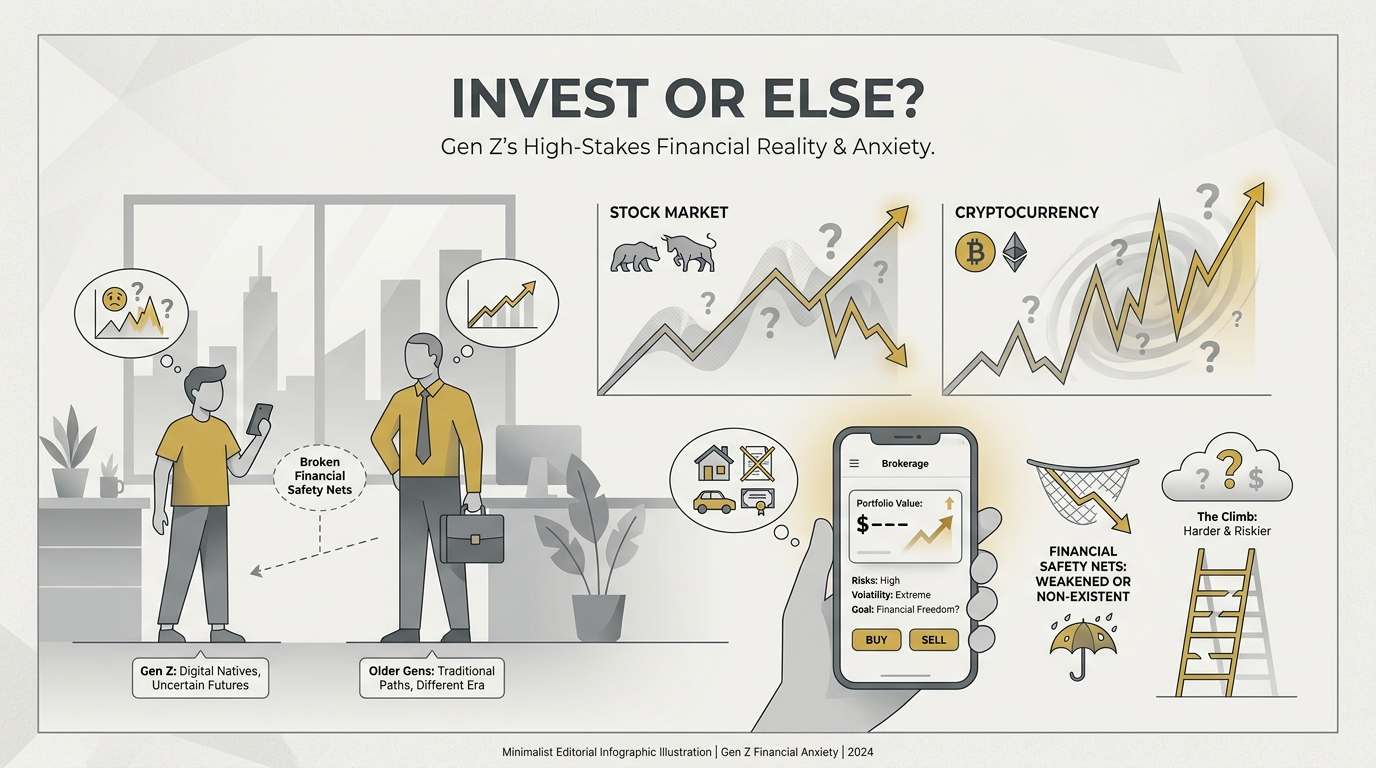

Picture a 24-year-old finishing her shift, pulling out her phone, and checking her investment portfolio before she even reads her messages. She is not investing because she feels optimistic about the future — she is investing because she is anxious about it.

24살 직장인이 퇴근 후 메시지 확인보다 먼저 투자 앱을 여는 장면을 떠올려 보세요. 그녀가 투자하는 이유는 미래에 대한 낙관이 아니라, 미래가 불안하기 때문이에요.

What's new

Gen Z Now Makes Up 22% of Retail Stock Trading

젠지가 소매 주식 거래의 22%를 차지해요

A new report shows that Gen Z investors — those born between 1997 and 2012 — now account for 22 percent of all retail stock trading in the United States. This is not driven by confidence in the economy, but by a deep mistrust of traditional safety nets like pensions and government benefits. In surveys, 64 percent of Gen Z investors cited "uncertainty about future income" as their primary motivation — far ahead of the 41 percent of older investors who said the same.

새 보고서에 따르면 젠지(1997~2012년생)는 현재 미국 소매 주식 거래의 22%를 차지하고 있어요. 이 급증세는 경제에 대한 자신감이 아니라, 연금이나 정부 지원 같은 전통적 안전망에 대한 깊은 불신에서 비롯되었어요. 설문에서 젠지 투자자의 64%가 "미래 소득에 대한 불확실성"을 주된 동기로 꼽았는데, 이는 같은 답을 선택한 기성 투자자 41%를 훨씬 웃도는 수치예요.

Why it matters

A Safety Net You Can't Trust Changes Everything

믿을 수 없는 안전망이 모든 것을 바꾸고 있어요

The US Social Security system is now projected to face as early as 2033, and younger workers are well aware that the math may not work in their favor. In South Korea, the story is strikingly similar: the number of brokerage accounts opened by people in their twenties and thirties grew by 42 percent between 2023 and 2025. At the same time, public trust in the National Pension Service hit a record low, as younger Koreans openly question whether they will ever receive the benefits they are paying into.

미국 사회보장제도는 이르면 2033년에 재정 고갈에 직면할 것으로 전망되고, 젊은 세대는 그 계산이 자신들에게 불리하다는 사실을 잘 알고 있어요. 한국 역시 상황이 매우 비슷해요. 2023년부터 2025년 사이 20~30대가 개설한 증권 계좌 수가 42%나 늘었어요. 동시에 국민연금에 대한 신뢰도는 사상 최저를 기록했고, 젊은 한국인들은 지금 납부하는 연금을 나중에 돌려받을 수 있을지 공개적으로 의문을 품고 있어요.

Context

High Risk, High Stakes: What Gen Z Is Actually Buying

고위험·고배당: 젠지가 실제로 사는 것들

Rather than putting money into bonds or index funds, Gen Z investors are concentrating their portfolios in individual stocks and cryptocurrency, which now represent 67 percent of their holdings. Platforms like Robinhood and South Korea's Toss have accelerated this trend by offering fractional shares, gamified dashboards, and near-zero transaction fees. These features have dramatically lowered the barrier to entry, drawing in users who would previously have considered investing out of their reach.

채권이나 분산 인덱스 펀드 대신, 젠지 투자자들은 개별 주식과 암호화폐에 집중하는 경향이 있는데, 이것이 이들 포트폴리오의 67%를 차지하고 있어요. 로빈후드나 한국의 토스 같은 플랫폼은 조각 주식 투자, 게임화된 대시보드, 거의 무료인 거래 수수료를 통해 이 흐름을 더욱 빠르게 키우고 있어요. 이런 기능들은 투자 문턱을 획기적으로 낮춰, 예전에는 투자가 자신과 거리가 멀다고 생각했을 사람들까지 시장으로 끌어들이고 있어요.

The bigger picture

The Risk Nobody Is Talking About

아무도 말하지 않는 리스크

Financial advisors warn that this concentration in high-risk assets could the damage of any future downturn, as a wave of young investors exits the market simultaneously. The deeper irony is that the very forces pushing Gen Z to invest — eroding safety nets and job insecurity — are the same forces that make their portfolios more fragile. Policymakers and financial educators are beginning to ask whether individual investing can truly substitute for a rebuilt social contract between governments and younger generations. Next time you open your investment app out of habit, pause for one honest question: are you investing with genuine optimism, or are you against a future you cannot quite believe in — because the answer to that question shapes every financial decision that follows.

재무 전문가들은 고위험 자산 집중이 미래 경기 침체 시 피해를 더욱 악화시킬 수 있다고 경고하는데, 젊은 투자자들이 동시에 시장에서 빠져나갈 경우 특히 위험해요. 더 깊은 아이러니는, 젠지를 투자로 내모는 바로 그 힘(무너지는 안전망, 불안정한 고용)이 동시에 그들의 포트폴리오를 더 취약하게 만든다는 점이에요. 정책 입안자들과 금융 교육자들은 이제 개인 투자가 정부와 젊은 세대 간의 새로운 사회 계약을 대신할 수 있는지 진지하게 묻기 시작했어요. 다음번에 습관처럼 투자 앱을 열 때, 한번 물어보세요. 당신은 희망을 품고 투자하는 건가요, 아니면 확신할 수 없는 미래를 대비하는 건가요?