Health Tech2026.05.02

The Pill That Could Replace the Shot: Pfizer's Oral GLP-1 Matches Injectable Weight Loss in Phase 3

주사를 대체할 알약: 화이자 경구용 GLP-1, 3상에서 주사제와 동등한 체중 감량 달성

Intro

The injection problem

주삿바늘이라는 장벽

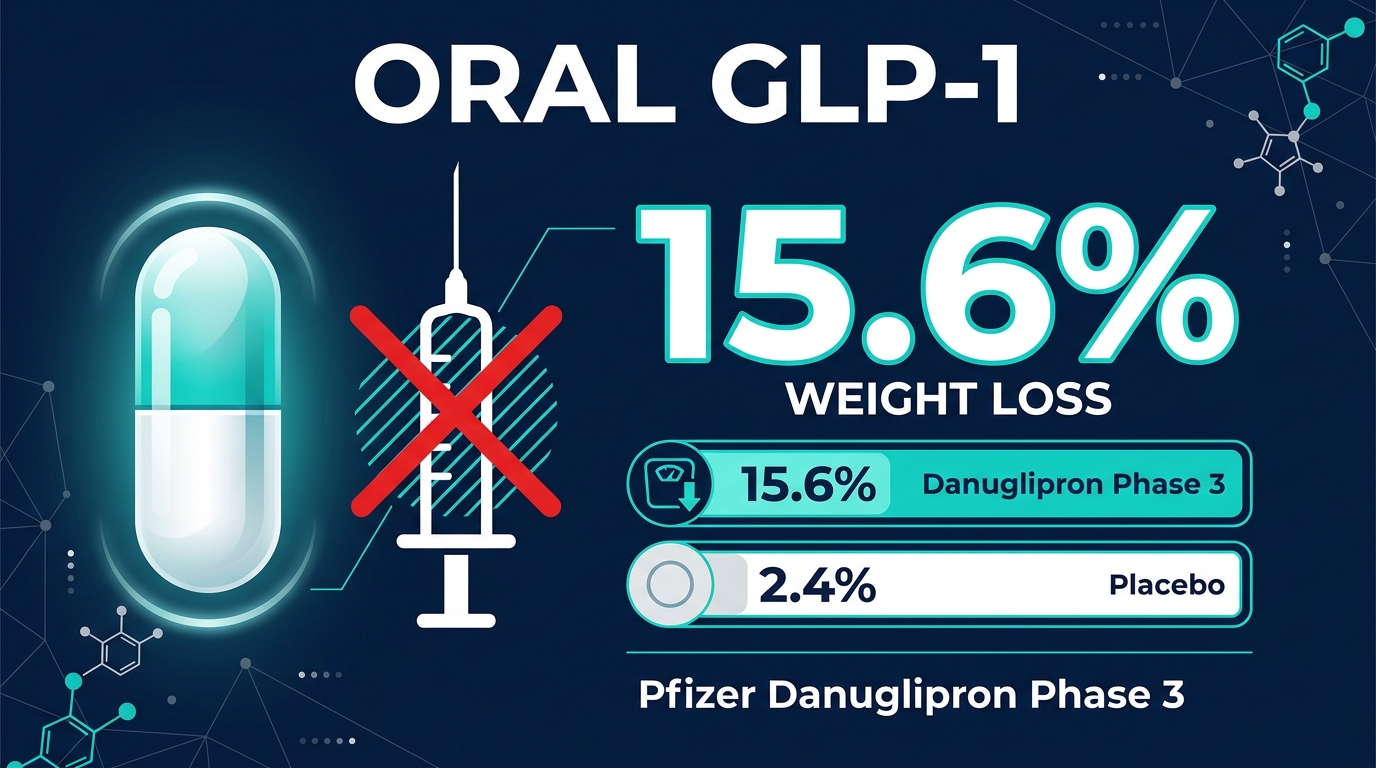

For millions of people living with obesity, the promise of GLP-1 medications — drugs like Wegovy and Ozempic that can produce dramatic weight loss — has come with a significant catch: you have to inject them yourself, once a week, with a needle. On May 2, 2026, Pfizer announced Phase 3 trial results for danuglipron — a once-daily pill that belongs to the same class of drugs as the injectable GLP-1 medications currently dominating the weight-loss market. The results showed that patients who took the pill lost an average of 15.6% of their body weight over 52 weeks, compared to just 2.4% in the group. That number is significant. Injectable semaglutide — the active ingredient in Wegovy — produces roughly 15 to 17% weight loss in similar trials. For the first time, an oral GLP-1 pill has matched the performance of its injectable counterpart at the same treatment duration, without requiring a single injection.

비만과 함께 살아가는 수백만 명의 사람들에게, 위고비(Wegovy)와 오젬픽(Ozempic)처럼 극적인 체중 감량을 가능하게 하는 GLP-1 계열 약물의 약속에는 중요한 조건이 하나 붙어 있었습니다. 바로 주 1회 스스로 주사를 놓아야 한다는 것입니다. 2026년 5월 2일, 화이자는 하루 한 번 복용하는 경구용 약물 다누글리프론(danuglipron)의 3상 임상시험 결과를 발표했습니다. 이 약물은 현재 체중 감량 시장을 주도하고 있는 주사형 GLP-1 계열 약물과 같은 계통에 속합니다. 결과에 따르면, 이 알약을 복용한 환자들은 52주 동안 평균 체중의 15.6%를 감량했으며, 이는 위약군의 2.4%에 비해 현저히 높은 수치였습니다. 이 수치는 중요한 의미를 지닙니다. 위고비의 주성분인 주사형 세마글루타이드(semaglutide)는 비슷한 임상시험에서 약 15~17%의 체중 감량 효과를 보입니다. 경구용 GLP-1 알약이 처음으로 동일한 치료 기간 내에 주사제와 동등한 성과를 달성한 것입니다. 단 한 번의 주사도 없이요.

How it works

What GLP-1 does — and why a pill changes everything

GLP-1의 작용 원리 — 그리고 알약이 모든 것을 바꾸는 이유

To understand why this is a big deal — and what GLP-1 drugs actually do in the body — it helps to start with the biology. GLP-1 stands for glucagon-like peptide-1, a hormone that your gut naturally releases after you eat a meal. It does several important things at once: it tells the pancreas to release insulin (to manage blood sugar), it slows down how quickly food leaves the stomach (so you feel full longer), and — critically — it signals to the brain that you are satisfied and should stop eating. GLP-1 receptor agonists are drugs that mimic this natural hormone but last much longer in the body — hours or days instead of minutes. The effect is that people taking these drugs feel less hungry, eat less, and over time, lose significant amounts of weight. For people with type 2 diabetes, the insulin-stimulating effect is also directly therapeutic. The existing injectable GLP-1 drugs — Wegovy and Ozempic, both versions of semaglutide made by Novo Nordisk, and Eli Lilly's tirzepatide (Zepbound) — have transformed obesity medicine since their approvals between 2021 and 2023. But the injection requirement has been a genuine barrier. Studies estimate that 30 to 40% of patients who could benefit from these medications decline them specifically because of needle aversion. There have been earlier attempts at oral GLP-1 drugs. Novo Nordisk's Rybelsus — an oral version of semaglutide — has been available since 2019, but it was approved only for type 2 diabetes, not obesity, and at doses that produced more modest weight loss. Danuglipron is the first oral GLP-1 candidate to achieve weight-loss efficacy that matches the injectable standard at the higher doses needed for obesity treatment.

이것이 왜 중요한 일인지, 그리고 GLP-1 약물이 실제로 체내에서 어떤 작용을 하는지 이해하기 위해서는 생물학적 메커니즘부터 살펴보는 것이 좋습니다. GLP-1은 글루카곤 유사 펩타이드-1(glucagon-like peptide-1)의 약자로, 식사 후 소화관에서 자연적으로 분비되는 호르몬입니다. 이 호르몬은 동시에 여러 중요한 역할을 합니다. 인슐린을 분비하도록 췌장에 신호를 보내고(혈당 조절), 위에서 음식이 비워지는 속도를 늦추며(더 오래 포만감을 느끼도록), 결정적으로 뇌에 포만 신호를 보내 식사를 그만해도 된다고 알려줍니다. GLP-1 수용체 작용제(receptor agonist)는 이 자연 호르몬을 모방하되 체내에서 훨씬 더 오래 지속되는 약물입니다. 몇 분이 아니라 몇 시간이나 며칠씩 유지됩니다. 그 결과, 이 약물을 복용하는 사람들은 덜 배고프고 덜 먹게 되며, 시간이 지나면서 상당한 체중 감량으로 이어집니다. 2형 당뇨병 환자에게는 인슐린 분비 촉진 효과 자체가 직접적인 치료 효과이기도 합니다. 기존의 주사형 GLP-1 약물들 — 노보 노디스크가 만든 세마글루타이드의 두 버전인 위고비와 오젬픽, 그리고 일라이 릴리의 티르제파타이드(Zepbound) — 은 2021년에서 2023년 사이 승인 이후 비만 의학을 혁신했습니다. 그러나 주사 요건은 실질적인 장벽이었습니다. 연구에 따르면, 이 약물의 혜택을 받을 수 있는 환자의 30~40%가 주삿바늘에 대한 거부감을 이유로 치료를 거부합니다. 경구용 GLP-1 약물 개발 시도는 이전에도 있었습니다. 노보 노디스크의 리벨서스(Rybelsus) — 세마글루타이드의 경구용 버전 — 가 2019년부터 시판되고 있지만, 비만이 아닌 2형 당뇨병에만 승인되었으며 더 적당한 수준의 체중 감량 효과를 보이는 용량으로 처방됩니다. 다누글리프론은 비만 치료에 필요한 고용량에서 주사제 기준에 필적하는 체중 감량 효과를 달성한 최초의 경구용 GLP-1 후보 물질입니다.

The trial

Phase 3 results: what the numbers show

3상 임상 결과: 숫자가 보여주는 것

In Pfizer's Phase 3 trial, 4,200 adults with a BMI of 27 or higher were assigned to receive either danuglipron or a once daily for 52 weeks. The danuglipron group lost a mean 15.6% of body weight. For someone weighing 100 kilograms (220 pounds) at baseline, that translates to losing approximately 15.6 kilograms — roughly the weight of a large bag of luggage. The most common side effects were gastrointestinal — nausea, vomiting, and diarrhea — reported by 24% of participants in the danuglipron group. This is the same category of side effects that GLP-1 injectables produce, though the rate was slightly lower than the 31% reported for injectable semaglutide in comparable trials. The side effects were mostly mild to moderate and typically resolved within the first eight weeks as the body adjusted to the drug. An oral pill changes the practical calculus of who can take these medications. Beyond needle aversion, there are patients who physically cannot self-inject due to limited dexterity, patients in regions where cold-chain drug storage (required for injectables) is unavailable, and lower-income patients for whom the convenience of a pill over a monthly prescription device matters for .

화이자의 3상 임상시험에서는 BMI 27 이상의 성인 4,200명이 52주 동안 하루 한 번 다누글리프론 또는 위약을 복용하도록 배정되었습니다. 다누글리프론 투여 그룹은 평균 15.6%의 체중을 감량했습니다. 기준 체중이 100kg인 사람의 경우, 약 15.6kg을 감량하는 셈으로, 이는 대형 여행 가방 하나 정도의 무게입니다. 가장 흔한 부작용은 위장관계 — 오심, 구토, 설사 — 로, 다누글리프론 투여군의 24%에서 보고되었습니다. 이는 GLP-1 주사제가 유발하는 것과 같은 계통의 부작용이지만, 비슷한 임상시험에서 주사형 세마글루타이드에 대해 보고된 31%보다 다소 낮은 비율입니다. 부작용은 대부분 경증 내지 중등도였으며, 신체가 약물에 적응하는 첫 8주 내에 대부분 해소되었습니다. 경구용 알약은 이 약물을 복용할 수 있는 사람들의 실질적인 계산법을 바꿉니다. 주삿바늘 거부감 외에도, 손의 민첩성 부족으로 자가 주사가 불가능한 환자들, 주사제에 필요한 콜드 체인(냉장 보관 유통망)이 없는 지역의 환자들, 그리고 알약의 편의성이 복약 순응도에 큰 영향을 미치는 저소득층 환자들이 존재합니다.

What it means

Market, access, and the economics of a pill

시장, 접근성, 그리고 알약의 경제학

Pfizer plans to file for FDA approval by Q3 2026, which would put a potential U.S. launch on track for sometime in 2027. The timeline aligns with several competing oral GLP-1 programs. Novo Nordisk is also running Phase 3 trials for a higher-dose oral semaglutide pill specifically targeting obesity, and Eli Lilly has an oral GIP/GLP-1 dual agonist in Phase 2. The race to an oral obesity pill is accelerating across the industry. The financial stakes are enormous. The injectable GLP-1 market reached approximately $35 billion in 2025 — and both Novo Nordisk and Eli Lilly have struggled to manufacture enough supply to meet demand. Analysts project the oral GLP-1 market alone could reach $60 billion by 2030 if multiple drugs receive approval, partly because pills are generally cheaper to manufacture and distribute than biological injectables. There is a broader access dimension worth understanding. GLP-1 medications currently cost between $900 and $1,300 per month in the United States without insurance coverage, and Medicare only began covering them for obesity in 2026 following significant lobbying. In most countries globally, insurance coverage for obesity drugs remains either non-existent or severely limited. An oral pill changes the manufacturing economics in ways that could — eventually — reduce costs. Injectable biologics require complex cell-culture manufacturing, specialized storage at specific temperatures, and single-use auto-injector devices. A small-molecule pill like danuglipron uses standard pharmaceutical tablet manufacturing. If generic competition enters within a decade, the price trajectory for oral GLP-1s could be dramatically different from that of injectables.

화이자는 2026년 3분기까지 FDA 승인 신청을 계획하고 있으며, 이는 잠재적인 미국 출시를 2027년 어느 시점으로 맞추게 됩니다. 이 일정은 여러 경쟁 경구용 GLP-1 프로그램과 맞물립니다. 노보 노디스크도 비만에 특화된 고용량 경구 세마글루타이드 알약의 3상 임상시험을 진행 중이며, 일라이 릴리는 경구용 GIP/GLP-1 이중 작용제를 2상에 두고 있습니다. 경구용 비만 치료제를 향한 경쟁이 업계 전반에서 가속화되고 있습니다. 재정적 판돈은 엄청납니다. 주사형 GLP-1 시장은 2025년 약 350억 달러에 달했으며, 노보 노디스크와 일라이 릴리 모두 수요를 충족할 만큼 충분한 공급을 제조하는 데 어려움을 겪어왔습니다. 애널리스트들은 경구용 GLP-1 시장 단독으로도 여러 약물이 승인될 경우 2030년까지 600억 달러에 달할 수 있다고 전망합니다. 부분적으로는 알약이 생물의약품 주사제보다 일반적으로 제조와 유통 비용이 저렴하기 때문입니다. 더 넓게 이해해야 할 접근성 차원이 있습니다. 현재 GLP-1 계열 약물은 미국에서 보험 적용 없이 월 900~1,300달러에 달하며, 메디케어(Medicare)는 상당한 로비 끝에 2026년에야 비만에 대한 적용을 시작했습니다. 전 세계 대부분의 국가에서는 비만 치료제에 대한 보험 적용이 없거나 극히 제한적입니다. 경구용 알약은 결국 비용을 낮출 수 있는 방식으로 제조 경제학을 바꿉니다. 주사형 생물의약품은 복잡한 세포 배양 제조 공정, 특정 온도에서의 전문 보관, 일회용 자동 주사기가 필요합니다. 다누글리프론과 같은 소분자 알약은 표준 제약 정제 제조 방식을 사용합니다. 10년 내로 제네릭 경쟁이 진입한다면, 경구용 GLP-1의 가격 궤적은 주사제와 극적으로 달라질 수 있습니다.

Patient action

Limits, risks, and a shift in how we understand obesity

한계, 위험, 그리고 비만을 바라보는 시각의 변화

Critics and cautious clinicians point out that while 15.6% weight loss is impressive, it remains below the 20–25% range achievable with tirzepatide (Eli Lilly's injectable dual agonist) at maximal doses, and well short of the 30–40% reductions seen after bariatric surgery. For patients with severe obesity and multiple comorbidities, those differences matter clinically. There are also open questions about long-term safety. GLP-1 drugs, both injectable and oral, are relatively new as obesity treatments — the longest-running trials span roughly five to six years. Rare but serious potential risks, including thyroid tumors observed in animal studies at very high doses, remain under active surveillance by regulators. The obesity medicine field is also grappling with a question that extends beyond pharmacology: what happens when patients stop taking GLP-1 drugs? Studies of both injectable and oral GLP-1s show that the majority of weight regained within 12 months of discontinuation. This rebound effect suggests these drugs may need to be taken indefinitely — a different mental model than, say, a course of antibiotics that you take and finish. That framing — obesity as a chronic condition requiring indefinite treatment rather than a short-term fixable problem — is itself a shift in medical understanding that GLP-1 drugs have helped drive. It parallels how the medical community came to view hypertension and high cholesterol: as conditions requiring long-term management with medication rather than conditions that medication can cure. Pfizer, which missed the first wave of the GLP-1 revolution — it had a prior oral GLP-1 program that failed in Phase 2 in 2023 — appears to have found a path back into the market with danuglipron's reformulated chemistry and higher-dose regimen. A successful FDA filing and approval would put Pfizer in direct competition with Novo Nordisk and Eli Lilly in the most commercially significant drug category of the decade. For patients watching this space, danuglipron represents something more tangible than a market event: it is a potential answer to the question that many people considering GLP-1 therapy have quietly asked — "is there a version of this I can just take as a pill?" Before switching to or starting any GLP-1 medication, ask your doctor to compare the injectable and oral options on your individual risk profile — because the convenience of a daily pill and the efficacy of a weekly injection are not interchangeable, and what works best depends on your specific health history.

비판적인 시각과 신중한 임상의들은 15.6%의 체중 감량이 인상적이기는 하지만, 최대 용량에서 일라이 릴리의 주사형 이중 작용제인 티르제파타이드로 달성 가능한 20~25% 범위에는 미치지 못하며, 비만 수술 후 나타나는 30~40% 감소에 훨씬 못 미친다고 지적합니다. 심각한 비만과 다발성 동반 질환을 가진 환자에게는 이 차이가 임상적으로 중요합니다. 장기 안전성에 관한 미해결 질문들도 있습니다. GLP-1 약물은 주사형과 경구형 모두 비만 치료제로서는 비교적 새로운 계통으로, 가장 오래 진행된 임상시험도 약 5~6년에 걸쳐 있습니다. 매우 고용량의 동물 연구에서 관찰된 갑상선 종양을 포함한 드물지만 심각한 잠재적 위험들은 규제 기관의 적극적인 감시 하에 있습니다. 비만 의학 분야는 약리학을 넘어서는 질문과도 씨름하고 있습니다. GLP-1 약물 복용을 중단하면 어떻게 될까요? 주사형과 경구형 GLP-1 모두의 연구에서, 복약 중단 후 12개월 내에 대부분의 체중이 다시 증가하는 것으로 나타납니다. 이러한 반동 효과는 이 약물들을 무기한 복용해야 할 수 있음을 시사하는데, 이는 항생제처럼 정해진 기간 복용하고 끝내는 방식과는 다른 인식 모델이 필요합니다. 비만을 단기간에 고칠 수 있는 문제가 아닌 무기한 치료가 필요한 만성 질환으로 보는 이 관점 자체가, GLP-1 약물이 이끌어 온 의학적 이해의 변화입니다. 이는 의학계가 고혈압과 고지혈증을 바라보게 된 방식과 유사합니다. 약물로 완치되는 질환이 아닌, 약물로 장기 관리해야 하는 질환으로 보게 된 것입니다. 2023년 2상에서 이전 경구용 GLP-1 프로그램이 실패하며 GLP-1 혁명의 첫 번째 물결을 놓쳤던 화이자는, 재설계된 화학 구조와 고용량 요법으로 다누글리프론과 함께 시장 복귀의 길을 찾은 것으로 보입니다. FDA 승인 신청과 승인에 성공한다면 화이자는 이 10년의 가장 상업적으로 중요한 약물 카테고리에서 노보 노디스크, 일라이 릴리와 직접 경쟁하게 됩니다. 이 분야를 주시하는 환자들에게, 다누글리프론은 단순한 시장 사건 이상의 구체적인 의미를 지닙니다. GLP-1 치료를 고려하는 많은 사람들이 조용히 던져 왔던 질문에 대한 잠재적인 답이기 때문입니다. "그냥 알약으로 먹을 수 있는 버전이 있나요?" 어떤 GLP-1 약물로 전환하거나 시작하기 전에, 주사제와 경구제 옵션을 여러분 개인의 위험 프로필에 맞게 비교해달라고 의사에게 요청하세요. 매일 복용하는 알약의 편의성과 주 1회 주사의 효능은 서로 교환 가능하지 않아요. 무엇이 가장 잘 맞는지는 여러분의 구체적인 건강 이력에 달려 있어요.